If you have lost your job, there are a number of tax issues you may encounter. How you deal with these issues can profoundly impact your taxes and finances. Watch this video to learn more about some typical issues.

.embed-container { position: relative; padding-bottom: 56.25%; height: 0; overflow: hidden; max-width: 100%; } .embed-container iframe, .embed-container object, .embed-container embed { position: absolute; top: 0; left: 0; width: 100%; height: 100%; }

Monthly Archives: October 2020

Gambling and Tax Gotchas

Article Highlights:

Winnings

Losses

Social Security Income

Health Care Insurance Premium Subsidies

Medicare B & D Premiums

Online Gambling Accounts

Gambling is a recreational activity for many taxpayers, and as one might expect, the government takes a cut if you win and won’t allow you to claim a loss in excess of your winnings. In fact, there are far more tax issues related to gambling than you might expect, and they may impact your taxes in more ways than you might believe. Here is a rundown on the many issues, the so-called ‘gotchas,’ that can affect you. Reporting Winnings – Taxpayers must report the full amount of their gambling winnings for the year as income on their 1040 returns. Gambling income includes, but is not limited to, winnings from lotteries, raffles, lotto tickets and scratchers, horse and dog races, and casinos, as well as the fair market value of prizes such as cars, houses, trips, or other non-cash prizes. The full amount of the winnings must be reported, not the net after subtracting losses. The exception to the last statement is that the cost of the winning ticket or winning spin on a slot machine is deductible from the gross winnings. For example, if you put $1 into a slot machine and won $500, you would include $499 as the amount of your gross winnings, even if you’d previously spent $50 feeding the machine. Frequently, taxpayers with winnings only expect to report those winnings included on Form W-2G. However, while that form is only issued for ‘Certain Gambling Winnings,’ the tax code requires all winnings to be reported. All winnings from gambling activities must be included when computing the deductible gambling losses, which is generally always an issue in a gambling loss audit.

GOTCHA #1 – Since you can’t net your winnings and losses, the full amount of your winnings ends up in your adjusted gross income (AGI). The AGI is used to limit other tax benefits, as discussed later. So, the higher the AGI, the more your other tax benefits may be limited.

Reporting Losses – A taxpayer may deduct gambling losses suffered in the tax year as a miscellaneous itemized deduction (not subject to the 2% of AGI limitation), but only to the extent of that year’s gambling gains.

GOTCHA #2 – If you don’t itemize your deductions, you can’t deduct your losses. Thus, individuals taking the standard deduction will end up paying taxes on all of their winnings, even if they had a net loss.

Social Security Income – For taxpayers receiving Social Security benefits, whether those benefits are taxable depends upon the taxpayer’s income (AGI) for the year. The taxation threshold for Social Security benefits is $32,000 for married taxpayers filing jointly, $0 for married taxpayers filing separately, and $25,000 for all other filing statuses. If the sum of AGI (before including any SS income), interest income from municipal bonds, and one-half the amount of SS benefits received for the year exceeds the threshold amount, then 50–85% of the SS benefit is taxable.

GOTCHA #3 – If your gambling winnings push your AGI for the year over the threshold amount, your gambling winnings—even if you had a net loss—can cause up to 85% of your Social Security benefits to become taxable.

Health Insurance Subsidies – Lower income individuals who purchase their health insurance from a government marketplace are given a subsidy in the form of a tax credit to help pay the cost of their health insurance. Most people eligible for the tax credit use it to reduce their monthly health insurance premiums. That tax credit is based upon the AGIs of all members of the family. The higher the family income, the lower the subsidy becomes.

GOTCHA #4 – The addition of gambling income to your family’s income can result in significant reductions in the health insurance subsidy, requiring you to pay more for your family’s health insurance coverage for the year. Additionally, if your subsidy was based upon your estimated income for the year, if your premiums were reduced by applying the subsidy in advance, and if you subsequently had some gambling winnings, then you could get stuck with paying back some or all of the subsidy when you file your return for the year.

Medicare B & D Premiums – If you are covered by Medicare, the amount you are required to pay (generally withheld from your Social Security benefits) for Medicare B premiums is normally $144.60 per month and is based on your AGI two years prior. However, if that AGI was above $87,000 ($174,000 for married taxpayers filing jointly), the monthly premiums can increase to as much $491.60. If you also have prescription drug coverage through Medicare Part D, and if your AGI exceeds the $87,000/$174,000 threshold, your monthly surcharge for Part D coverage will range from $12.20 to $76.40 (2020 rates).

GOTCHA #5 – The addition of gambling winnings to your AGI can result in higher Medicare B & D premiums.

Online Gambling Accounts – If you have an online gambling account, there is a good chance that the account is with a foreign company. All U.S. persons with a financial interest or signature authority over foreign accounts with an aggregate balance of over $10,000 anytime during the prior calendar year must report those accounts to the Treasury by the April due date for filing individual tax returns or face draconian penalties.

GOTCHA #6 – Regardless of whether you are a gambling winner or loser, if your online account was over $10,000, you will be required to file FinCEN Form 114 (Report of Foreign Bank and Financial Accounts), commonly referred to as the FBAR. For non-willful violations, civil penalties up to $10,000 may be imposed; the penalty for willful violations is the greater of $100,000 or 50% of the account’s balance at the time of the violation. The $10,000 and $100,000 penalty amounts are subject to adjustment for inflation, and after February 19, 2020 are $13,481 and $134,806, respectively.

Other Limitations – The aforementioned are the most significant ‘gotchas.’ Numerous other tax rules limit tax benefits based on AGI, as discussed in gotcha #1. These include medical deductions, certain casualty losses, child and dependent care credits, the Child Tax Credit, and the Earned Income Tax Credit, just to name a few. If you have questions related to gambling and taxes, please call this office.

Is a Living Trust Appropriate for You?

Article Highlights:

What Is a Living Trust?

Is a Living Trust Appropriate?

Establishing a Living Trust

Pros of a Revocable Trust

Cons of a Revocable Trust

You have probably heard others discussing living trusts but may not understand the reasons for them or whether you should have one. Living trusts are an estate-planning tool, and there is not a one-type-fits-all living trust. Each one is customized to suit the special circumstances of the individual for whom it was created. The vast majority of the population can get by without using a living trust, and a simple will is perfect for most people, unless their estate is large or there are some special circumstances to deal with. There actually are two types of these trusts: revocable and irrevocable. As the names imply, an irrevocable trust generally cannot be undone once made, while the provisions of a revocable trust can be changed or rescinded as long as the grantor (the individual who established the trust) is still living. A living trust becomes irrevocable when the grantor passes. Because an irrevocable trust would only be established under very special circumstances, they aren’t discussed in this article. While you can designate your beneficiaries in either a will or a living trust, there are some things that only one document or the other can do. So, even if you create a living trust, you may still need a will. Because these are legal documents, it is probably best to have the assistance of an attorney in preparing them, although do-it-yourself software does exist. Yes, you’ll have to pay legal fees to have the work done by a lawyer, but the cost of a professional’s expertise oftentimes will pay for itself by having all the I’s dotted and T’s crossed. Unfortunately, these legal fees aren’t tax-deductible. When a living trust is established, generally, all of an individual’s assets are assigned to the trust, including the home, rentals, stock accounts, bank accounts, etc. However, while living, the grantor still gets the use and benefit of these assets, just as if the living trust had not been established, and income and capital gains derived from assets in the trust are reported on the individual’s 1040 and state (if applicable) tax returns. As part of the process of setting up the living trust, the assets placed into the trust will need to be retitled into the trust’s name. Generally, the benefits of a living trust outweigh the negative implications. Here is a condensed rundown of the pros and cons of a living trust: Some of the Pros of a Revocable Trust: Avoid Probate – Probate is the legal process through which the court ensures that, when an individual dies, their debts are paid and their assets are distributed according to the individual’s will, if there is one, or in accordance with state law if there’s no will or trust. Upon the grantor’s death, all of the assets held in the revocable trust bypass probate, meaning they pass to the grantor’s beneficiaries without having to go through the often time-consuming and expensive probate court process. Probate can take a long time, and the proceedings are a public process. Maintain Control of Assets after Death – A living trust can include provisions to delay distributions to children until they reach a specific age and to help protect assets from falling into the hands of creditors or an ex-spouse. Distributions can be designed to fit the heirs’ circumstances. Reduce the Possibility of a Court Challenge – A living trust is often more difficult to challenge than a will because it is harder to prove incompetence. Prevent Conservatorship – If the grantor becomes incapacitated, then a living trust can protect the family from undergoing a conservatorship process. A conservatorship is when a court-appointed representative is given the authority to manage an incapacitated person’s financial matters for them. Instead, with a living trust, if the grantor ever reaches the point where they are unable to manage their own affairs, a successor trustee who is already named in the trust by the grantor will step in. That trustee has a fiduciary responsibility to manage the trust’s assets for the grantor’s benefit. Some of the Cons of a Revocable Trust: Additional Paperwork – A disadvantage of a living trust is the additional paperwork required in assigning ownership of the grantor’s assets to the trust. To be fully effective, the ownership of all of the grantor’s property must be legally transferred to the “grantor as the trustee.” If an asset has a title (e.g., real estate, stocks, mutual funds), then the title should be changed to show that the property is now owned by the trust. No Tax Benefits – Shifting assets to a revocable trust does not save income or estate taxes. Until the trust becomes irrevocable upon the grantor’s death, the grantor is still responsible for all tax issues related to assets included in the trust. Thus, the grantor should continue to implement appropriate tax strategies. Lacks Asset Protection – Assets held within a revocable trust are treated as being owned by the grantor and are within the reach of creditors. Difficulty Refinancing Trust Property – Since the legal title of real estate is held in the trustee’s name, some banks and title firms may balk if the grantor wants to refinance the property. Providing a copy of the trust document, which specifically gives the grantor, as trustee, the power to borrow against the trust’s property, should satisfy their concerns. Otherwise, it may be necessary to remove the asset from the trust temporarily by retitling it in the grantor’s own name and then reversing the procedure once the refinancing has been completed. If you have general questions related to living trusts, please give this office a call.

VIDEO: Unable to Keep Up with Your Home Mortgage Payments?

If you are receiving temporary home mortgage relief under the CARES Act or in danger of having your home repossessed, know that any debt relief can have an impact on your taxes. Watch this video to find out more.

.embed-container { position: relative; padding-bottom: 56.25%; height: 0; overflow: hidden; max-width: 100%; } .embed-container iframe, .embed-container object, .embed-container embed { position: absolute; top: 0; left: 0; width: 100%; height: 100%; }

Local SEO: What Factors Affect Your Local Search Rankings?

How can tax and accounting practices rank higher for local search results?

It all comes down to focusing on a combination of the most influential local SEO ranking factors. Google’s algorithm for local search is fluid and complex, so it can be difficult to know where to spend your time and resources to improve your chance for high ranks.

It’s getting harder and harder to rank on search as a local business. The SEO landscape has changed, and it’s not just the major nationwide brands who are optimizing for search; local SEO is becoming more competitive as well.

2020 Key Local Ranking Factors

At their recent Local Search Summit (September 2020), Whitespark announced the initial findings of their latest Local Search Ranking Factors survey. The insights they shared can help local businesses like CPAs, EAs, and tax and accounting firms to prioritize which aspects to allocate resources to.

These were the most important ranking factors for local pack and localized organic rankings in 2020, based on Whitespark’s report:

Local Pack

- Google My Business (33%)

- Reviews (16%)

- On-Page & Links (15% – tie)

- Behavioral (8%)

- Citations (7%)

- Personalization (6%)

Local Organic

- On-Page (32%)

- Links (31%)

- Behavioral (10%)

- Google My Business & Personalization (7% – tie)

- Citations & Reviews (6% – tie)

These rankings were based on what local search experts said were the most important ranking factors to local pack and localized organic results.

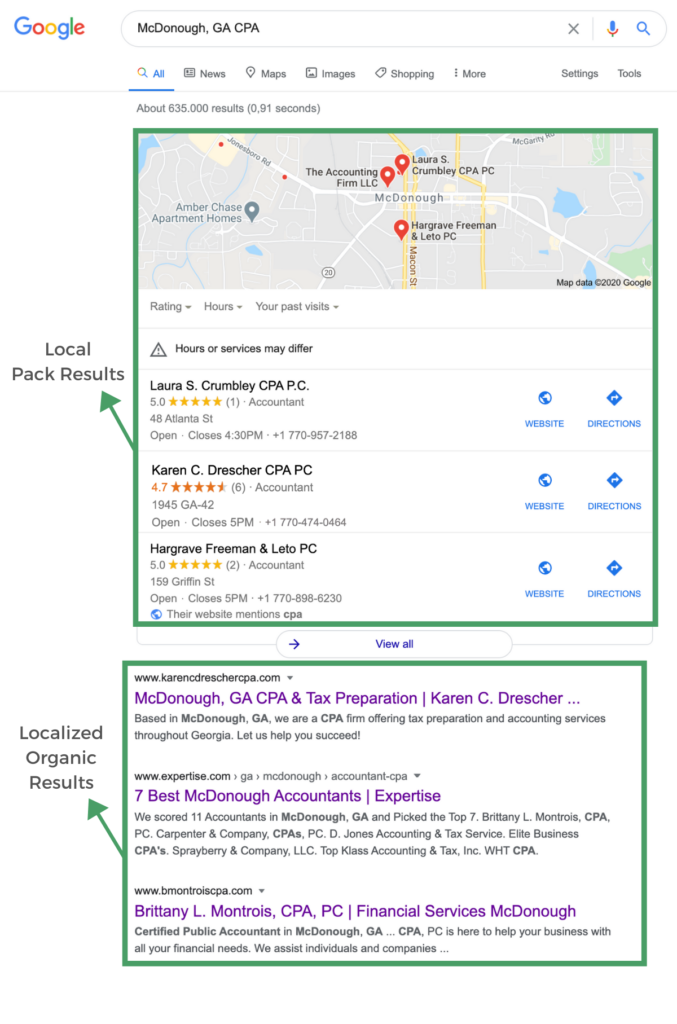

For reference, “local pack” and “local organic” are referring to these types of search results:

BrightLocal averaged out the the combination of both factors for those businesses who are looking to improve their rankings in both:

- On-page optimization (24%)

- Links (23%)

- GMB (20%)

- Reviews (11%)

- Behavioral (9%)

- Citations & Personalization (7% – tie)

Remember: prioritization is never as simple as just dividing your time/efforts up by these exact percentages. Some of the factors are more time-intensive and others can be outsourced.

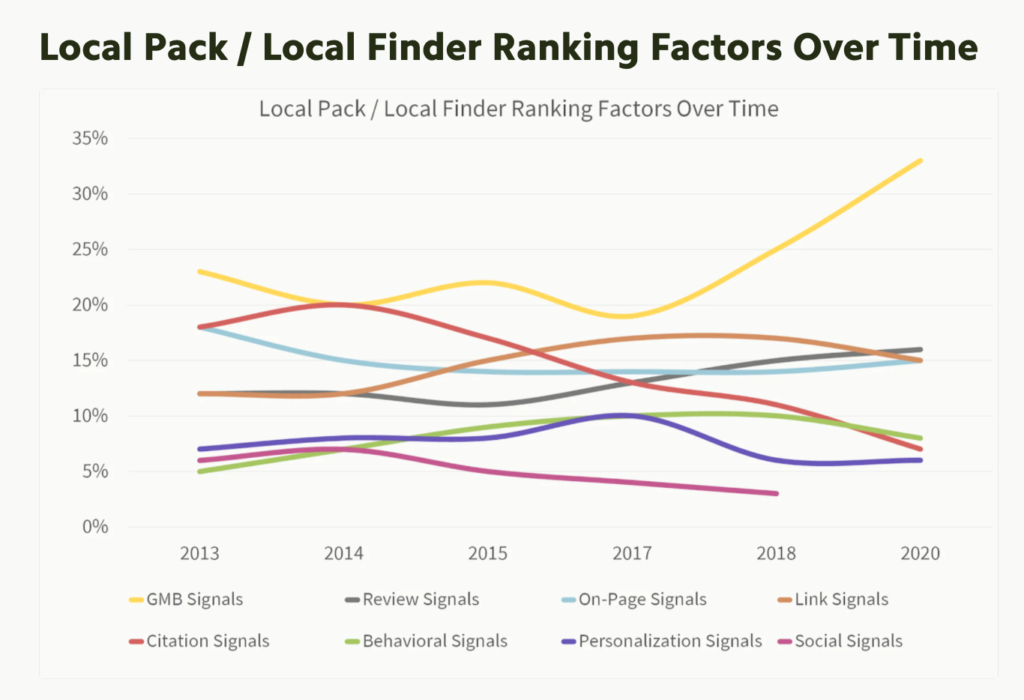

Trends of Local Ranking Factors Over Time

As Google’s algorithms change over time, it can be helpful to look at how the significance of local ranking factors evolve as well. This chart, also from BrightLocal, clearly indicates the exponential growth of Google My Business (GMB) Signals and their influence on local rank.

As you can see, GMB signals have remained the most important factor since 2013 – and by even higher margins since 2017. This is, of course, unsurprising: Google wants businesses to use their products, so they make it almost impossible to succeed in search without GMB.

That being said, it’s actually a positive for businesses. GMB is one more place to get your brand in front of consumers, and it’s often in the moment when they’re searching for services like yours – aka when they have purchase intent.

It’s imperative to keep your GMB listing optimized on an ongoing basis. 64% of consumers have used GMB listings to find a local business’s address or phone number, and GMB is the 2nd most trusted source to find accurate and up-to-date contact information (behind only the business’s website).

How CountingWorks PRO Can Improve Practices’ Local Search Rankings

Most of the most important factors for Local Pack and Localized Organic results can be improved through your CountingWorks PRO subscription without needing to lift a finger.

As mentioned above, GMB is crucial to your SEO success as a local business – and it’s one of our specialties.

We will claim your GMB listing and work with you to verify your practice locations. Then, our team optimizes the content of your listing, ensuring your list of services, name/address/phone number, and other business information is accurate and consistent. We also lock in your data so outside users cannot touch your information, update your data for you as needed, and connect your GMB listing to your website.

Additionally, we’ll create logo and cover images for you to give your listing a professional look. With our Social Pro add-on, we provide frequent automated blog posting to your GMB to improve the quality of your listing, and we offer done-for-you review campaigns to drive customer reviews for your listing.

If you’d like to learn more about our SEO and GMB services, or have questions about local search factors and how to improve your rankings, contact us today at 1-800-442-2477 x3 or set up some time to speak with one of our digital marketing experts.

The post Local SEO: What Factors Affect Your Local Search Rankings? appeared first on Website and Marketing Automation Software for Accountants | CountingWorks PRO.

Solar Tax Credit is Sunsetting Soon

Article Highlights:

Solar Credit Phasing Out

Qualifying Property

When is the Credit Available?

Who Gets the Credit

Multiple Installations

Battery

Installation Costs

Basis Adjustment

Association or Cooperative Costs

Mixed-Use Property

Newly Constructed Homes

Utility Subsidy

Solar Installations are Not for Everyone

A federal tax credit for the purchase and installation costs of a residential solar system is fading away. After being 30% of the cost for several years through 2019, the credit amount drops to 26% in 2020 and then 22% in 2021, the final year of the credit. The credit is non-refundable, meaning it can only reduce an individual’s tax liability to zero. However, the portion of credit that is not allowed because of this limitation may be carried to the next tax year and added to the credit allowable for that year. The tax code infers that any credit carryover can be added to the credit allowed in the subsequent year. However, what is unclear is whether any carryover will be allowed to 2022 once the credit expires at the end of 2021. In addition to the credit reducing the regular tax, it also reduces the alternative minimum tax should a taxpayer be subject to it. Qualifying Property – Only the following solar power systems are eligible for the credit:

Qualified solar electric property – property that uses solar energy to generate electricity for use in a home that is the taxpayer’s main or second residence.

Qualifying solar water heating property – qualifies if used in a dwelling located in the U.S. that is used by the taxpayer as a main or second residence where at least half of the energy used to heat water is derived from the sun. Heating water for swimming pools or hot tubs does not qualify for the credit. The solar equipment must be certified for performance by the Solar Rating Certification Corporation or a comparable entity endorsed by the state government where the property is installed.

When Is the Credit Available? – The credit may be claimed on the tax return of the year during which the installation is completed, so if a taxpayer has purchased and paid for a system and it is completed in 2020, the credit will be 26% of the cost. But if the project isn’t completed until 2021, the credit will only be 22%. This becomes an even a bigger issue for systems being installed during 2021 that aren’t completed before 2022, when the credit rate will be zero. If you plan to purchase a solar system in 2021, the purchase should be made early enough in the year to ensure the installation is completed before 2022. Who Gets the Credit – It may come as a surprise, but the taxpayer need not own the residence where the solar property is installed to qualify for the credit, as the taxpayer need only be a “resident” of the home. The tax code does not specify that an individual has to own the home, only that it is the taxpayer’s residence. For example: A son lives with his mother, who owns the home. The son pays to have the solar system installed; the son is the one who qualifies for the credit. Multiple Installations – The credit is available for multiple installations. For instance, after the initial installation, if a taxpayer adds additional panels to increase capacity, these would be treated as original installations and qualify for credit at the credit rate applicable for the year the additional installation is completed, provided that the installation is done before 2022. On the other hand, if a taxpayer had to replace damaged panels or perform other maintenance on the system, these items would not be an original system and their costs would not qualify for the credit. Battery – A battery qualifies for the credit if it’s charged only by solar energy and not off the grid. This has become popular in areas where there are frequent power outages. However, this may be more of a convenience than a necessity, so carefully consider the cost. A software-management tool—whether part of the original installation or added later (before 2022)—also qualifies for the credit in cases in which the software is necessary to monitor the charging and discharging of solar energy from a battery attached to solar panels. Installation Costs – Amounts paid for labor costs allocable to onsite preparation, assembly, or original installation of property eligible for the credit, and for piping or wiring connecting the property to the residence, are expenditures that qualify for the credit. This includes expenditures relating to a solar system installed on a roof or ground-mounted installations. Basis Adjustment – The term basis is generally the cost of a home plus improvements and is the amount subtracted from the sales price to determine the gain or loss when the home is sold. The cost of a solar system adds to a home’s basis, and the credit reduces the basis. This will generally create a different basis for federal and state purposes where a state does not provide a solar credit or it differs from the federal solar credit amount. Association or Cooperative Costs – A taxpayer who is a member of a condominium association for a condominium they own, or a tenant-stockholder in a cooperative housing corporation, is treated as having paid their proportionate share of any qualifying solar system costs incurred by the condo or cooperative association or corporation. Mixed-Use Property – In cases where a portion of a residence is used for deductible business use or is rented to others, the expenses must be prorated and only the personal portion of the qualified solar costs can be used to compute the credit. There is an exception when less than 80% of the property is used for non-business purposes, in which case the full amount of the expenditures is eligible for the credit. Newly Constructed Homes – If you are planning on purchasing a newly constructed home that includes a solar system, you may be entitled to claim the solar credit. However, to do so, the costs of the solar system must be separate from the home construction costs and certification documents must be available. Utility Subsidy – Some public utilities provide a nontaxable subsidy (rebate) to their customers for the purchase or installation of energy-conservation property. In that case, the cost of the solar system that’s eligible for the credit must be reduced by the amount of the nontaxable subsidy that was received. Solar Installations are Not for Everyone – There are TV ads, telemarketing phone calls and sales people at your front door all promoting the benefits of solar power, and one of the key considerations and a frequently mentioned benefit is the federal tax credit. What isn’t included in the ads—and something most potential buyers are unaware of—is that the solar credit is a nonrefundable tax credit, meaning the credit can only be used to offset your tax liability. This can come as a very unpleasant surprise and is often a financial hardship when the purchaser of a home solar system finds out that the credit is nonrefundable and that they won’t benefit from the full credit. For example, a married couple with three children, all under age 17, and an annual income of $80,000 installed a solar system costing $20,000 in 2020, expecting a $5,200 ($20,000 x 26%) credit on their tax return. Their standard deduction in 2020 is $24,800, leaving them with a taxable income of $55,200. The tax on the $55,200 is $6,229. They are also entitled to a $2,000 child tax credit for each child, which reduces their tax liability by $6,000 and results in a tax liability of $229. Since the solar credit is nonrefundable, the only portion of the credit they can use is $229, not the $5,200 they had expected. On top of that, the family is probably financing the solar system, which significantly adds to the system’s cost. If the entire $20,000 cost were financed by a 5% home equity loan for 20 years, then the interest on that loan over its term would be $11,678, bringing the total cost of the solar system to $31,678 or a monthly cost of $132. In lieu of purchasing a solar system, some homeowners opt to lease a system. This arrangement is not eligible for the solar credit. As you can see, there is a lot to consider before making the final decision to install a solar system. Is it worth it, and is it the right financial move for you? Please call for a consultation before signing any contract to make sure a solar system is appropriate for you.